Executive Summary

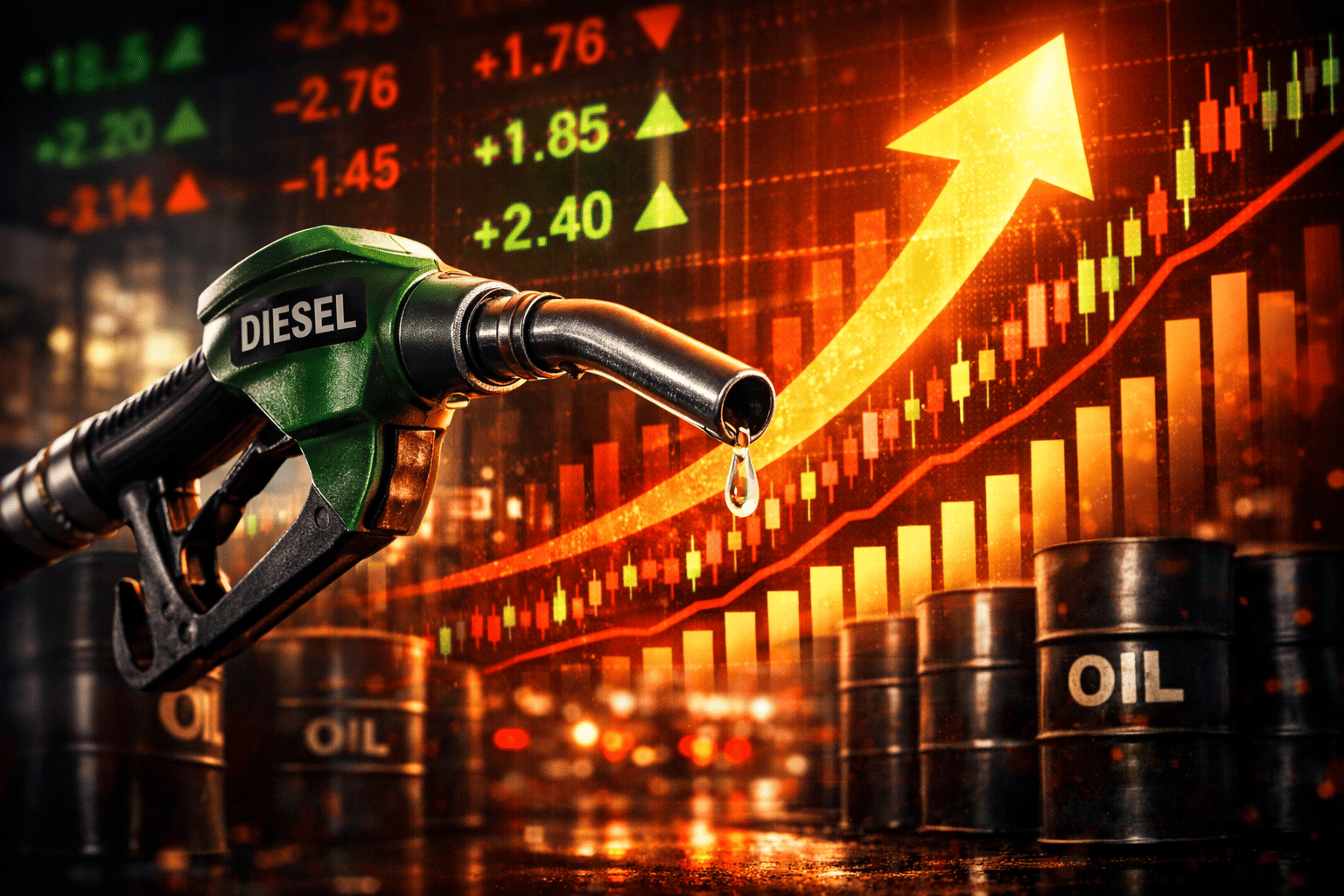

- Record Retail Prices: Petrol has breached ₹128/litre in Mumbai and ₹124/litre in Delhi, while diesel has crossed ₹115/litre in major metros—the highest nominal prices in Indian history.

- Global Crude Surge: Brent crude has surged past $102/barrel driven by OPEC+ supply constraints, Red Sea shipping disruptions, and geopolitical risk premiums in the Middle East.

- Tax Architecture Trap: Central excise duties and state VAT collectively account for 52–58% of retail fuel prices, leaving the government with minimal fiscal room to provide relief without blowing the deficit.

- Inflation Cascade: Transport and logistics costs have risen 20–25% since January, transmitting fuel price pressure into food, manufacturing, and core CPI with alarming speed.

The arithmetic of India's fuel economy has turned hostile. For a country that imports more than 87% of its petroleum requirements, the global oil market is not an abstract commodity exchange—it is the single most important external determinant of domestic inflation, fiscal health, and political stability. In April 2026, that external determinant has become a severe liability. Retail fuel prices across Mumbai, Delhi, Chennai, and Bangalore have surged to historic highs, triggering a cascading repricing of transport, logistics, and agricultural input costs that is reverberating through every layer of the economy. The fuel price explosion is not a temporary spike. It is a structural shock.

The proximate cause is a volatile cocktail of geopolitical risk and deliberate supply constraint. But the underlying condition is structural: India remains dangerously exposed to the vicissitudes of global hydrocarbon markets at a time when those markets are becoming less predictable, more politically weaponized, and increasingly disconnected from pure demand fundamentals. The question confronting New Delhi is not whether prices will moderate in the near term, but whether the economy can adapt to a prolonged era of expensive energy without triggering a broader macroeconomic crisis.

The Global Oil Shock Driving India's Fuel Price Explosion

International crude markets entered 2026 on a knife edge, and the first quarter has done nothing to restore equilibrium. Brent crude futures, the benchmark that dictates India's import economics, have traded in a destabilizing range between $91 and $104 per barrel, with the current settlement hovering near $102. This is not merely a price level; it is a volatility regime. The CBOE Crude Oil Volatility Index has spiked to levels last seen during the 2022 supply panic, reflecting deep uncertainty among traders about the stability of physical flows and the durability of OPEC+ production policy.

The supply side of the equation is being deliberately constricted. OPEC+, led by Saudi Arabia and Russia, has maintained aggressive production cuts of approximately 2.2 million barrels per day into the second quarter of 2026, citing the need to stabilize markets amid uncertain demand growth from China and India. In reality, the strategy appears designed to maximize fiscal revenues for producer nations ahead of a potential long-term demand plateau driven by electric vehicle adoption and renewable energy expansion. For import-dependent economies like India, this is a direct transfer of wealth from consumers to sovereign producers.

Compounding the OPEC+ strategy is the escalating risk premium in the Middle East. Attacks on commercial shipping in the Red Sea and Strait of Hormuz have forced tanker operators to reroute vessels around the Cape of Good Hope, adding up to 14 days to voyage times and dramatically increasing freight costs. Insurance premiums for hull and cargo coverage on Gulf-Asia routes have quadrupled since January. These are not abstract market frictions; they are direct cost escalators that land on the Indian consumer's bill at the petrol pump. Every rupee of freight and insurance premium is transmitted, through the import parity pricing mechanism, into the retail price of petrol and diesel.

"We are no longer pricing oil based on marginal cost of production. We are pricing it based on geopolitical risk, strategic scarcity, and the fiscal desperation of producer states. That is a fundamentally more expensive paradigm for import-dependent economies like India."

India's Fuel Price Architecture: Why the Consumer Pays So Much

Understanding the pain at the pump requires dissecting the tax and pricing mechanics that govern India's petroleum sector. The retail price of petrol and diesel in India is a layered construct: the base price reflects the international import parity, to which freight, insurance, refinery margins, dealer commissions, and excise duties are added, followed by value-added tax levied by individual states. In most major metros, taxes constitute between 52% and 58% of the final retail price. This architecture creates a rigid transmission mechanism that amplifies the impact of global crude spikes.

When international crude rises, the base price rises—and because taxes are often levied as fixed duties on top of a higher base, the consumer feels a magnified impact. Conversely, when the government reduces excise duties to provide relief, it sacrifices revenue that funds infrastructure, welfare schemes, and debt servicing. The fiscal trade-off is brutal and politically explosive. In November 2021 and May 2022, the Centre cut excise duties by ₹13 and ₹8 per litre respectively, sacrificing approximately ₹2 trillion in annual revenue. Those cuts have not been reversed, but they have also not been expanded, leaving the government with minimal fiscal room for further relief.

The deregulation narrative, which posits that retail prices move freely with market signals, has become increasingly strained in practice. While oil marketing companies technically have pricing autonomy, political sensitivities around fuel inflation have led to extended periods of price freeze followed by sharp, politically timed corrections. This stop-start dynamic has distorted consumer behavior, depleted marketing margins, and undermined the investment case for downstream infrastructure. The consumer, meanwhile, faces a double burden: high prices when global markets rise, and no relief when the government chooses fiscal consolidation over voter comfort.

Economic Ripple Effects: From Pump to Plate

The macroeconomic consequences of sustained high fuel prices are cascading through India with alarming speed. Transport and logistics, which account for roughly 14% of GDP, are experiencing severe cost inflation. Road freight rates have risen by 20–25% since January, as fleet operators pass through diesel costs to shippers. For a manufacturing economy that relies heavily on road transport for last-mile connectivity, this is a direct compression on margins and competitiveness. The cost of moving a tonne of goods from Mumbai to Delhi has increased by approximately ₹1,200, a cost that is ultimately borne by consumers across every product category.

Agriculture is equally exposed. Diesel powers irrigation pumps, tractor operations, and the cold-chain logistics that move perishables from farm to market. With diesel crossing ₹115/litre, the cost of cultivating a hectare of wheat or rice has risen by an estimated ₹4,200–₹5,100, at a time when farmgate prices remain politically constrained by minimum support price policies. The result is a squeeze on rural incomes that threatens to reverse the modest consumption recovery seen in late 2025. For the 45% of Indians still dependent on agriculture, the fuel price explosion is not an abstract economic indicator; it is a direct assault on livelihood viability.

| Economic Sector | Primary Impact | Cost Escalation (2026) | Policy Vulnerability |

|---|---|---|---|

| Household Transport | Direct fuel expenditure; two-wheeler and car operating costs surge. | Petrol up 16% YoY; CNG up 11%. | Political backlash in urban constituencies; demand destruction in vehicle sales. |

| Road Freight | Diesel-driven logistics inflation across manufacturing and retail. | Freight rates up 20–25% since January. | Margin compression for MSMEs; pass-through resistance in competitive sectors. |

| Agriculture | Irrigation, tillage, and cold-chain cost inflation; rural income squeeze. | Per-hectare cultivation cost up ₹4,200–₹5,100. | Fertilizer subsidy overlap; MSP pressure ahead of kharif season. |

| Aviation | ATF prices at record highs; ticket inflation and route rationalization. | ATF up 29% YoY; average fares up 22%. | Airline balance sheet stress; potential consolidation triggers. |

| Power Generation | Fuel oil and natural gas costs for peaking plants. | Power purchase costs up 14% for discoms. | Tariff hike resistance; discom financial stress. |

The Fiscal and Political Dilemma

For the Ministry of Finance, the fuel price crisis presents a trilemma with no painless resolution. Option one: maintain current excise rates and allow retail prices to rise, containing the fiscal deficit but stoking inflation and political anger. Option two: slash central excise duties by ₹8–₹12 per litre, providing immediate consumer relief but blowing a ₹1.6 trillion hole in the revenue account. Option three: reintroduce explicit subsidies, shielding consumers entirely but resurrecting the fiscal chaos of the pre-2014 era and undermining the credibility of pricing reform.

The government has thus far opted for a variant of option one, accompanied by symbolic gestures: minor duty adjustments, appeals to states to reduce VAT, and rhetorical pressure on oil marketing companies to absorb margin pain. None of these measures has materially altered the price trajectory. Meanwhile, the Consumer Price Index has breached 6.4% in the fuel and light category, complicating the Reserve Bank of India's inflation targeting mandate and reducing the probability of monetary easing in the second half of the year. With core inflation also elevated, the RBI faces the unenviable choice of hiking rates to contain inflation or holding steady to protect growth—either way, the fuel price explosion constrains policy space.

The political timeline adds urgency. With key state elections scheduled for late 2026 and the general election cycle visible on the horizon, the ruling coalition faces intense pressure to deliver visible relief. History suggests that Indian governments rarely withstand sustained fuel price inflation without eventually sacrificing fiscal discipline. The only question is the timing and scale of the intervention. A pre-election excise cut appears increasingly likely, despite the fiscal cost, as the political price of inaction exceeds the economic price of revenue sacrifice.

Energy Security and the Long Road to Resilience

Beyond the immediate price crisis lies a deeper strategic vulnerability: India's energy security architecture is not designed for a world of persistent supply disruption and volatile prices. The country maintains strategic petroleum reserves (SPRs) at three underground cavern facilities—Visakhapatnam, Mangalore, and Padur—with a combined capacity of approximately 39 million barrels, equivalent to roughly 9.5 days of net imports. While this provides a limited buffer against short-term supply shocks, it is grossly insufficient for a prolonged geopolitical conflict or sustained OPEC+ constraint.

The longer-term response has focused on diversification. India has aggressively expanded crude sourcing from non-OPEC suppliers, including the United States, Brazil, Guyana, and Canada, and has deepened energy diplomacy with Russia through discounted Urals crude purchases. However, discounted Russian barrels come with their own complications: payment mechanism frictions, insurance and shipping bottlenecks, and the ever-present risk of Western secondary sanctions that could freeze transactions overnight. The share of Russian crude in India's import basket has risen to approximately 38%, a concentration that creates its own vulnerabilities.

The electric vehicle transition, often cited as the ultimate escape route from oil dependence, remains structurally constrained. EV penetration in the passenger vehicle segment has reached only 7.2%, while the two-wheeler and commercial fleet segments—where fuel demand is most concentrated—remain overwhelmingly dependent on internal combustion. Charging infrastructure is patchy outside Tier-1 cities, and the power sector's own dependence on imported coal means that electrification merely shifts the import burden rather than eliminating it. The fuel price explosion of 2026 is a stark reminder that India's structural dependence on imported hydrocarbons will persist for at least another decade, regardless of transition rhetoric.

The Path Forward: Survival Strategies for Consumers and Policymakers

As India navigates the remainder of 2026, the fuel price explosion is unlikely to abate unless global crude markets experience an unexpected demand collapse or a geopolitical de-escalation that unlocks spare production capacity. Neither scenario appears probable. The more realistic outlook is a sustained period of elevated prices, punctuated by volatility spikes, that will test the resilience of Indian households, businesses, and government finances alike.

The policy imperative is clear, if politically difficult. In the short term, the government must target relief with surgical precision: direct cash transfers to vulnerable households, expanded public transport subsidies, and temporary freight rate stabilization mechanisms for essential commodities. In the medium term, the fiscal architecture around petroleum taxation needs structural reform, moving toward a transparent, floating duty mechanism that absorbs volatility rather than amplifying it. And in the long term, the only durable solution is acceleration of the energy transition—not merely electrification of transport, but a comprehensive decarbonization of industry, agriculture, and power generation that reduces India's structural dependence on imported hydrocarbons.

For consumers, the fuel price explosion demands immediate adaptation. Vehicle ownership patterns are already shifting, with demand surging for CNG, hybrid, and electric alternatives. Carpooling, public transport adoption, and remote work arrangements are reducing per-capita fuel consumption in urban areas. These are rational responses to a price signal that is unlikely to reverse. The fuel price explosion of 2026 is not a temporary aberration. It is a forewarning of the economic and strategic costs of energy dependence in an increasingly fragmented and volatile world. The question is whether India can adapt before the next shock arrives.